Credo Technology: Transformation or Desperation?

Credisne? Credo in my credo.

“Credisne?” (Do you believe?), said my Latin teacher, as we debated a point in a dead language, but one that gave birth to many. Over the years I became a lexicophile or philologist because I appreciate the subtlety and power in language, much less a single word. For most Credo Technology (CRDO) investors, right now it is all in its name.

Credo, Latin for “I believe”, in English is “any system of principles that guide a person or group.” Either applies today after the company, CRDO, reported earnings yesterday after the close; whether it is a statement or a question is the answer. But first some context. This post is for those already familiar in the name, as the AI train has already left the station.

Disclaimer: Taking a page from Monish Pabrai’s “shamelessly cloning” mantra, this post is an aggregation from various sources like Nikhs, BEP Research and my own frameworks.

Credo Technology (CRDO), the AI copper cable king, has had a good year; up over 120%. Its Q2 FY’26 call last November was a barnburner (highlights below):

The “Inflection Point”: CEO Bill Brennan officially stated that the company had reached the long-awaited revenue inflection point, citing “even greater momentum than initially projected.”

Customer Diversification: Management highlighted strong demand from their top two customers but, crucially, noted an “emerging third hyperscaler” that was beginning to scale, reducing the company’s reliance on Amazon (their historically dominant customer).

AEC (Active Electrical Cables) Dominance: The 50G and 100G per-lane AEC solutions were the primary drivers, as hyperscalers shifted toward denser AI clusters where AECs began displacing more expensive optical solutions for short-reach connections.

Product Launches: Credo launched its 800G ZeroFlap AECs, designed specifically to eliminate “link flaps” (connection drops) in massive AI training clusters, a major pain point for data center operators.

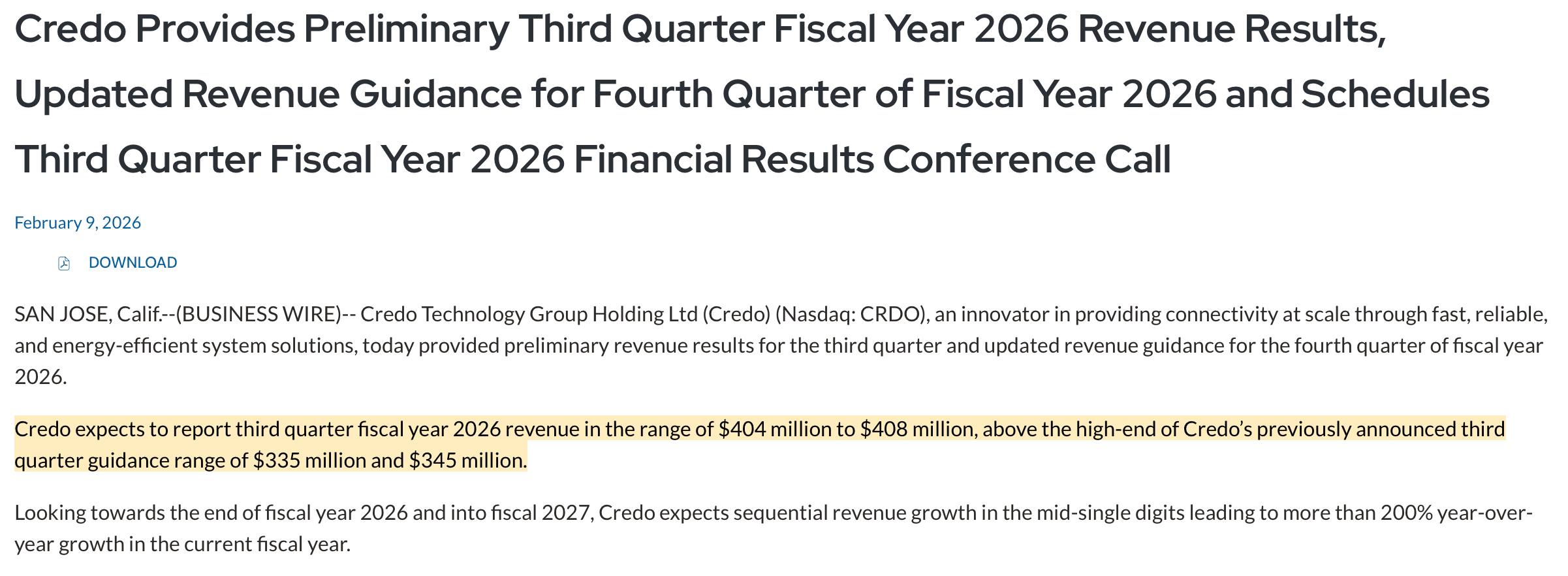

Momentum and sentiment was high for good reason. Then (not so) curiously, on February 9th, CRDO “pre-announced” earnings which usually means the company wishes to notify shareholders/analysts that their upcoming results may differ materially then previously thought.

The highlighted portion noted a 19% beat in revenue; but more importantly CRDO guided for “sequential revenue growth in the mid digits (for FY 2026)”. Shares were up 10% that day. Perhaps some of the bulls were so giddy at the revenue beat that the most important statement of decelerating top line growth and a multiple re-rating was seemingly ignored. This is probable. Our Levels of Thinking construct suggests 1st and 2nd order thinkers piled in to create a top, one that more measured investors saw as potential “Peak Copper Moment”.

Below is a lightly redacted screenshot from the I/O Discord CRDO channel. My somewhat cryptic missive is meant to signal my “credo” that a large move in price is imminent. Now most semi investors have known the photonics transition has been underway for a while now. But it’s my credo that most don’t confirm if the ultimate arbiter of truth here (stock price) reflected that.

Having tracked CRDO for a while, my take over a year ago was the CRDO would be one of the top AEC players in the space. Second order thinking suggested that because an accelerating AI product timeline would likely mean copper’s dominance would be shorter than our usual holding period (years), so we passed on CRDO as a long term investment.

A year ago this month, we hedged our semi portfolio on CRDO earnings. The rationale was covered in my post “The Drop in Credo Technology Group (CRDO) . . . is Justified: The Valuation Knife Cuts Both Ways”. The noise from expected business cashflow and metric fluctuations in an evolving field is answered/remedied with volatility when trillions of dollars are exchanged over guesses and incentives.

The thesis then was at some point CRDO was going to get re-rated or commoditized if they remained primarily a copper interconnect play. Yet the story and the company’s trajectory shifted as CEO Bill Brennan’s credo is to build the backbone or foundational connectivity for AI datacenters. Copper, gallium or indium phosphide, the material does not matter, they want to be the best to connect the rest. Their OmniConnect offering is the focus and will be mentioned later. My mindset also shifted from using them as a signpost (and portfolio hedge) for the optical crossover to tracking them as a potential long-term investment.

This takes us to their Q3 FY’26 report yesterday afternoon.

Top line was a pre-announced 19% beat on previous guidance. Huge bottom line beat but fueled by ultra-low effective tax rate. Clean balance sheet not including Comira acquisition announced yesterday.

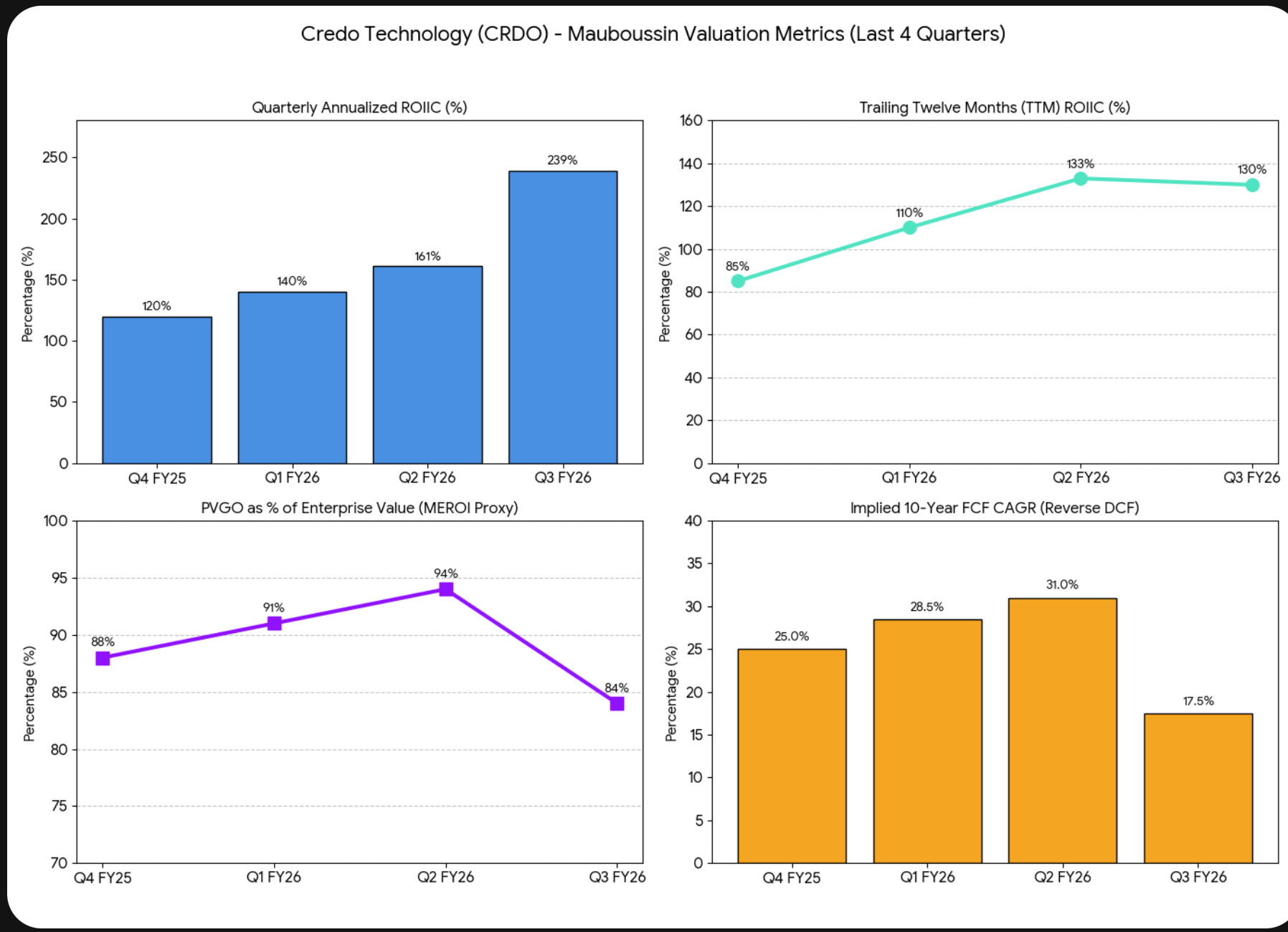

The Mauboussin ROIIC lens also looking strong:

CRDO’s performance demonstrated not only the pricing power of its AEC components due to market (hyperscaler) demand but also a possible technological moat. Credo’s credo in energy effectiveness and lower cost of ownership appears to be fueled by their system management features that more importantly offer superior reliability and operability.

But the other half of the lens points to what may be feeding market fear and the reasonable doubt in today’s extended sell-off. 2nd and 3rd order thinking points to a “Peak Copper” quarter and significant execution risks from the optical transition.

Below we see both the bull and the bear cases laid out:

Bulls point to quarterly ROIIC numbers that are accelerating to a fever pitch (239% in Q3), CRDO is the copper king of AECs; this is indisputable. However, looking at the TTM ROIIC trend, the sequential flattening from 133% to 130% would be the bears’ (and reasonable bulls’) indication that barring an instantaneous catalyst/pivot, CRDO’s growth HAS TO decelerate.

In fact, it had already started. Post Q2 earnings, CRDO price topped out at all time highs in the $210s and just prior to the Feb. 9th earnings pre-announcement saw an almost 50% nadir into the $110s. Yes, some macro dynamics and geo-political concerns can be included but directionally and by magnitude, this was not uncalled for. The pre-announcement also told us that sequential revenue would be up ~52% for Q3 but plummet to mid single digits for Q4. If this is unfamiliar territory for you, please reference my latest TTD post on how the math works.

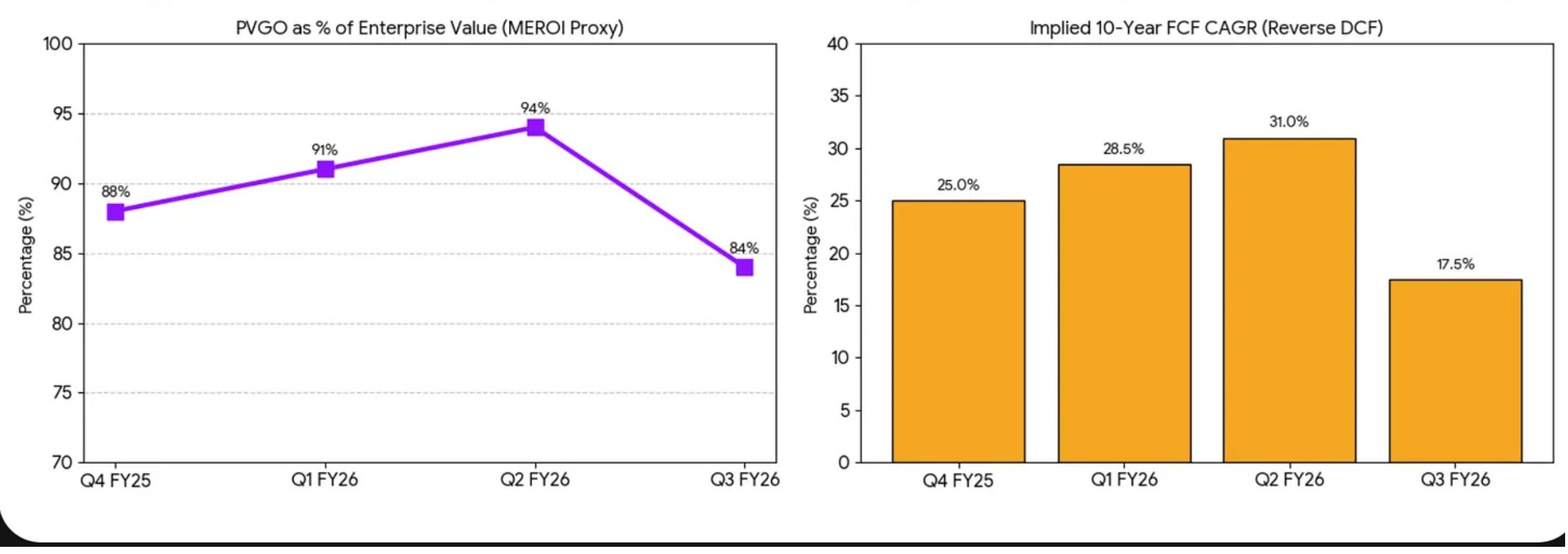

As for the other half of the Mauboussin metrics (PVGO) and its implications (Implied 10 year FCF CAGR), note that the expectations are still high but have been somewhat derisked since. More on that with my takeaways later.

And the fun is just beginning! Nvidia’s aqui-hire of Groq (“Nvidia Checkraises the Competition: Jensen Does It Again”) has been better understood as their move to differentiate their inference offerings by redefining the architectural overlay and going around the “memory wall”. Obviously this will pressure ASICs startups/peers (Broadcom (AVGO)/Marvell (MRVL)) and adjacents (Arista Networks (ANET)) . One of the 4th level observations I did not include was that if it is less likely that inference will cannibalize Nvidia GPUs, this should also be relatively bullish for current beneficiaries like Astera Labs (ALAB) and Credo.

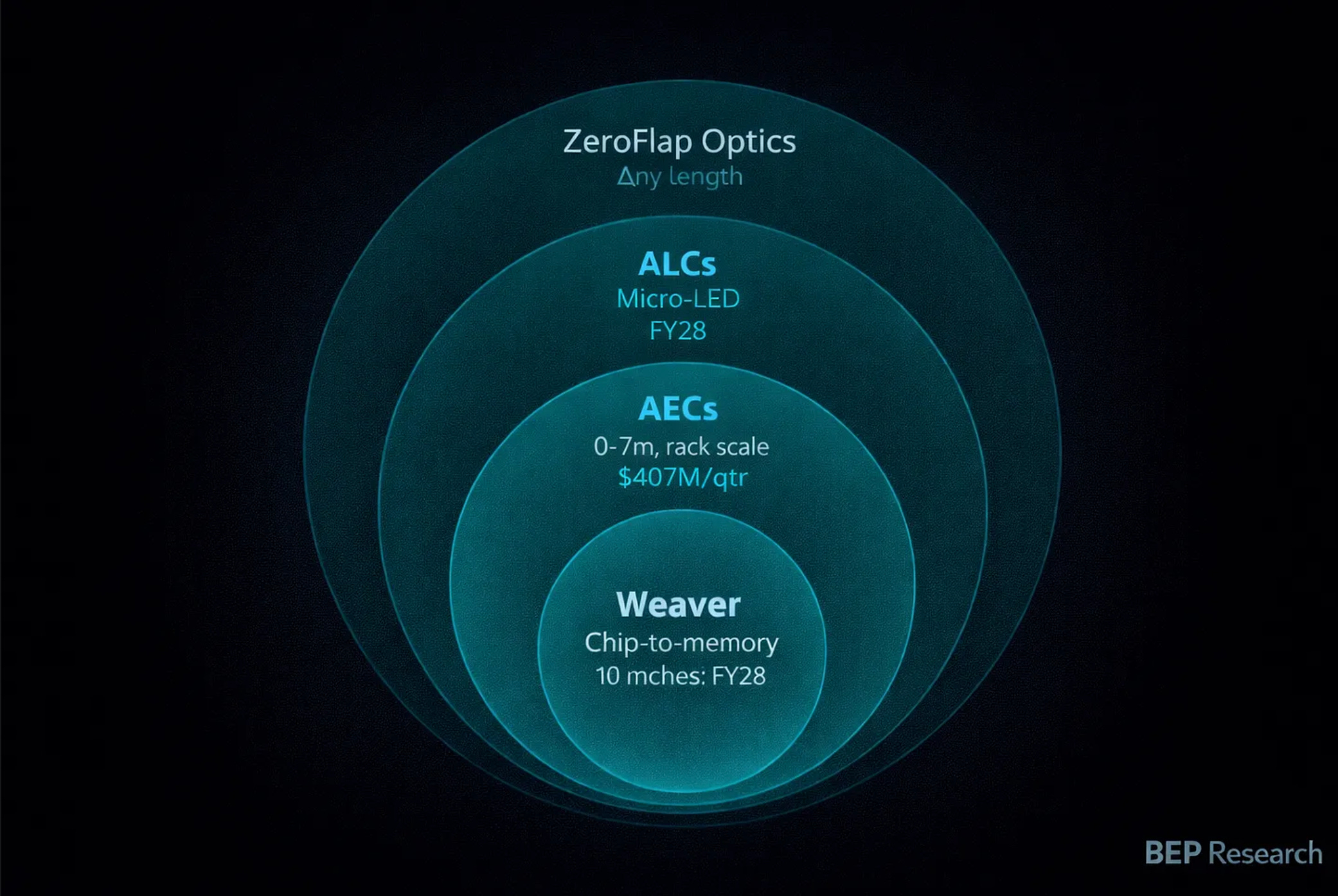

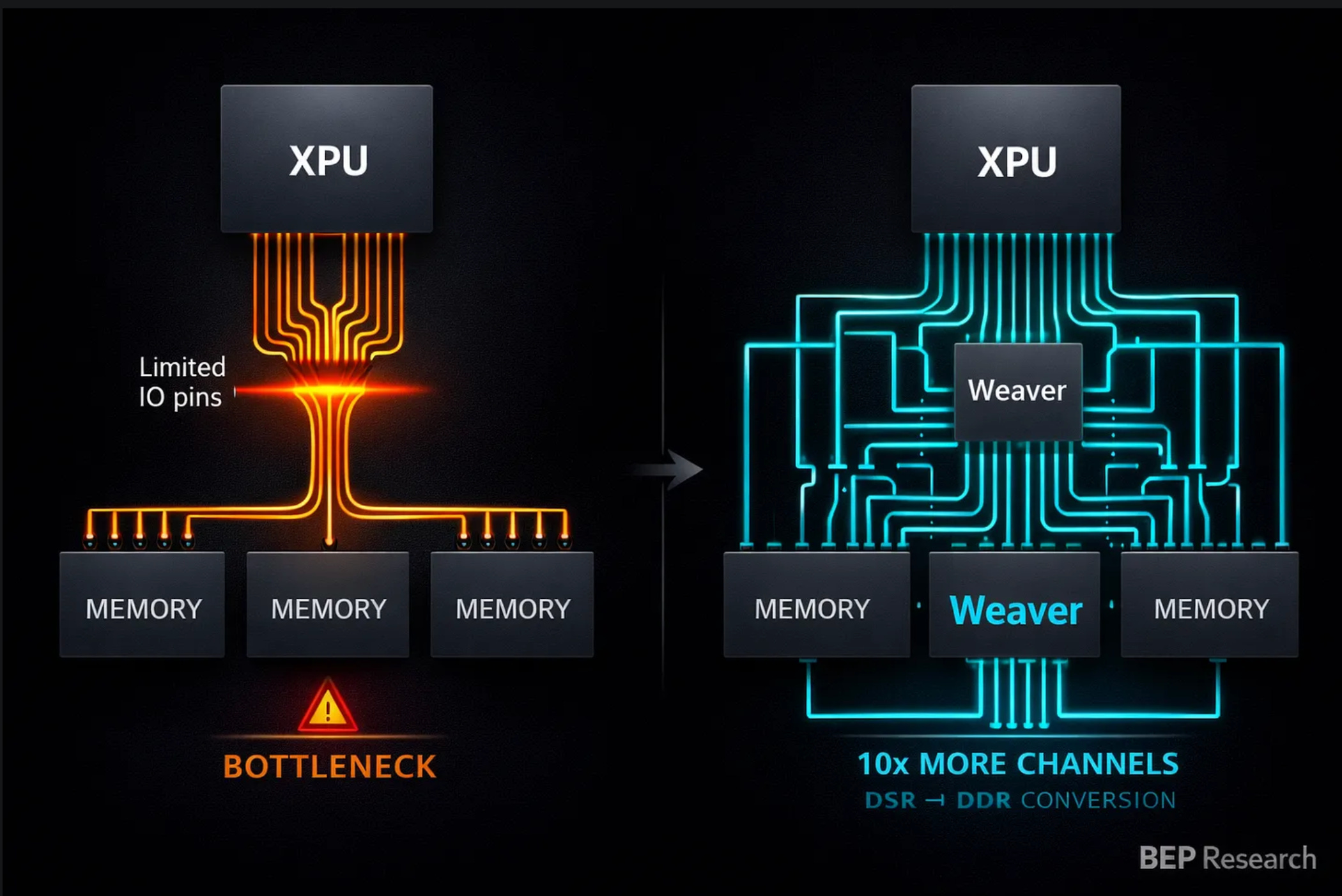

Then yesterday, Nvidia announced their $4B funding for Lumentum (LITE) and Coherent (COHR) optical buildouts. Jensen, IMO had thrown down the gauntlet with the Groq “compiler” and further laid out their intentions as CRDO shares continued to be pressured into the close. Their conference call also had what I would term CEO Brennan’s equivalent of a (smaller but company significant) gauntlet tossing with the announcement that their OmniConnect plans included the acceleration of their ZeroFlap optics from 2028 to this May, 2 months from now.

Ben Pouladian, founder of BEP Research, just wrote about OmniConnect, CRDO’s full datacenter connectivity stack yesterday (he’s an incredible follow, soon going to paid subscription):

Their first product, Weaver is worth reading about. Technology is the material expression of innovation. Credo’s credo again on display.

So where does that leave us and why the extended price drop today? We have a fantastic company executing at an elite level who has dominated the AEC interconnection space to create a differentiated offering that has not yet been commoditized. Now they are vying as David with the multi-trillion dollar Goliaths in what BEP Research has called “The Memory Wars”.

Going to reference another Substacker, Nikhs, as again his take is similar to mine but my implementation differs somewhat. This also would serve as a TL:DR/summary to this point:

Financial Strength vs. Market Fear: Despite reporting record revenue ($407 million, up 200% year-over-year) and exceptional 68.6% gross margins, the stock fell 12%. This disconnect reflects market anxiety that Credo’s “copper-heavy” business model is nearing a structural end.

The Threat of Co-Packaged Optics (CPO): Investors fear that as AI clusters move toward 1.6 terabit ports, light will inevitably replace copper. The concern is that NVDA and other hyperscalers will integrate optics directly into silicon, potentially turning Credo’s Active Electrical Cables (AECs) into a “melting ice cube.”

Pivot to “Managed Reliability”: Credo is attempting to decouple its value from the physical medium. By accelerating the production of ZeroFlap optical transceivers, the company is trying to prove that its PILOT telemetry software (which monitors link health) is just as essential for optical connections as it is for copper.

Margin Durability Debate: Credo’s high margins suggest it behaves more like an infrastructure company than a commodity hardware vendor. However, there is a looming question of whether these margins will compress as the product mix shifts from copper to more expensive optical components. Management has signaled a 300 to 400 bps decrement but margins remain in the mid 60s.

The Hyperscaler Risk: The long-term thesis hinges on whether Credo’s reliability layer remains proprietary. History shows that hyperscalers (like Amazon and Google) often eventually build or commoditize external networking solutions once they reach a certain scale. I do agree that the technical intensity and detail of this may favor Credo, though.

Nikhs’ 6 signposts are thoughtful and very reasonable. As with my current Broadcom consilience article that is active (earnings tomorrow), we will see how this plays out. Next I would like to explain why the sell-off deepened today.

Due to time constraints, below are screenshots from my in-house quant, GDR (Gemini Deep Research) =), where we used the $114 after hours stock price to construct a sensitivity table.

MEROI (Market-Expected Return on Investment)

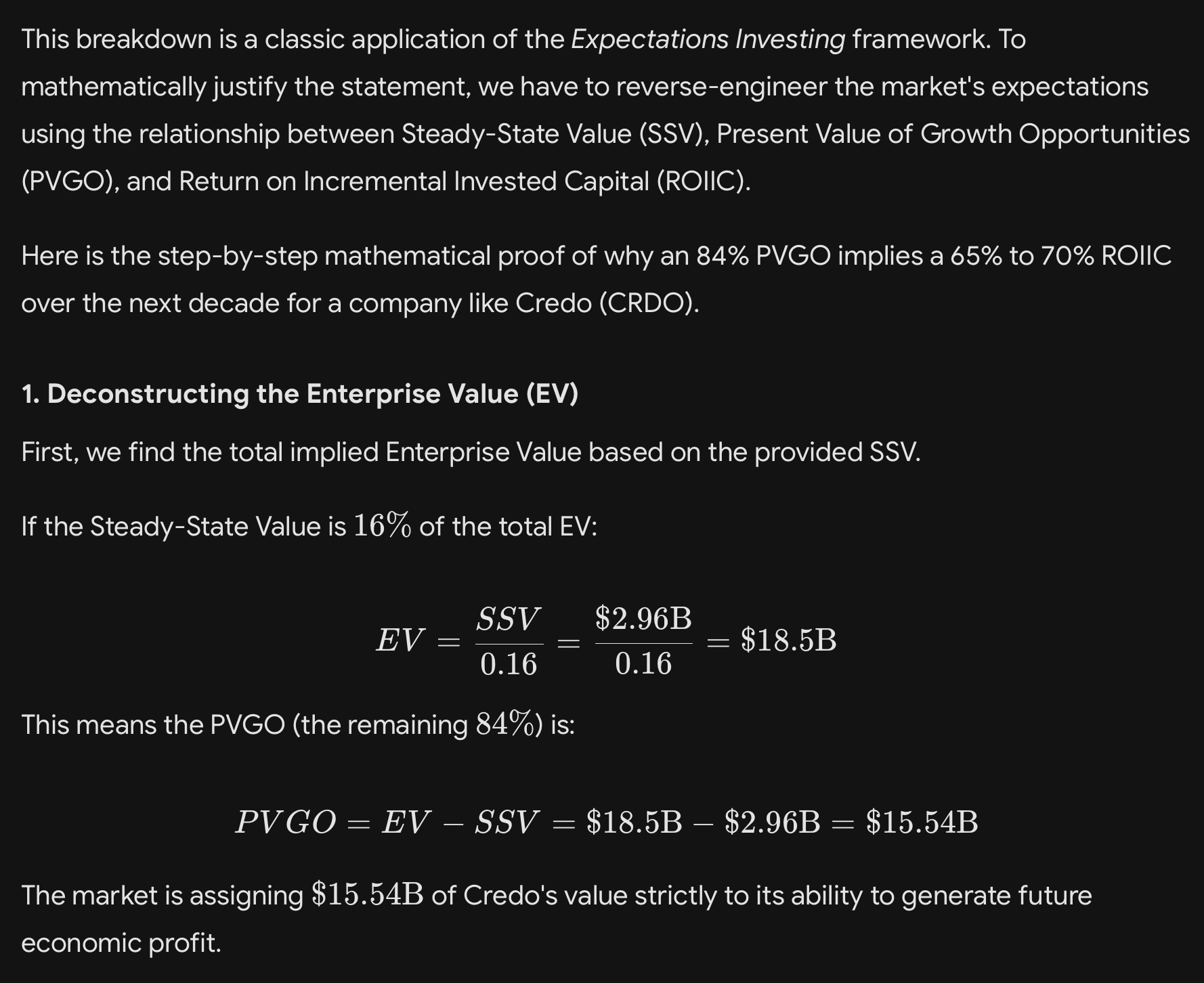

Mauboussin uses MEROI to parse a company’s Enterprise Value (EV) into two buckets: the value of the business as it stands today, and the value the market is assigning to future growth.

Enterprise Value: At ~$114/share with 180.6M shares, Market Cap is $20.06B. Subtracting $1.3B in cash leaves an EV of $18.76B.

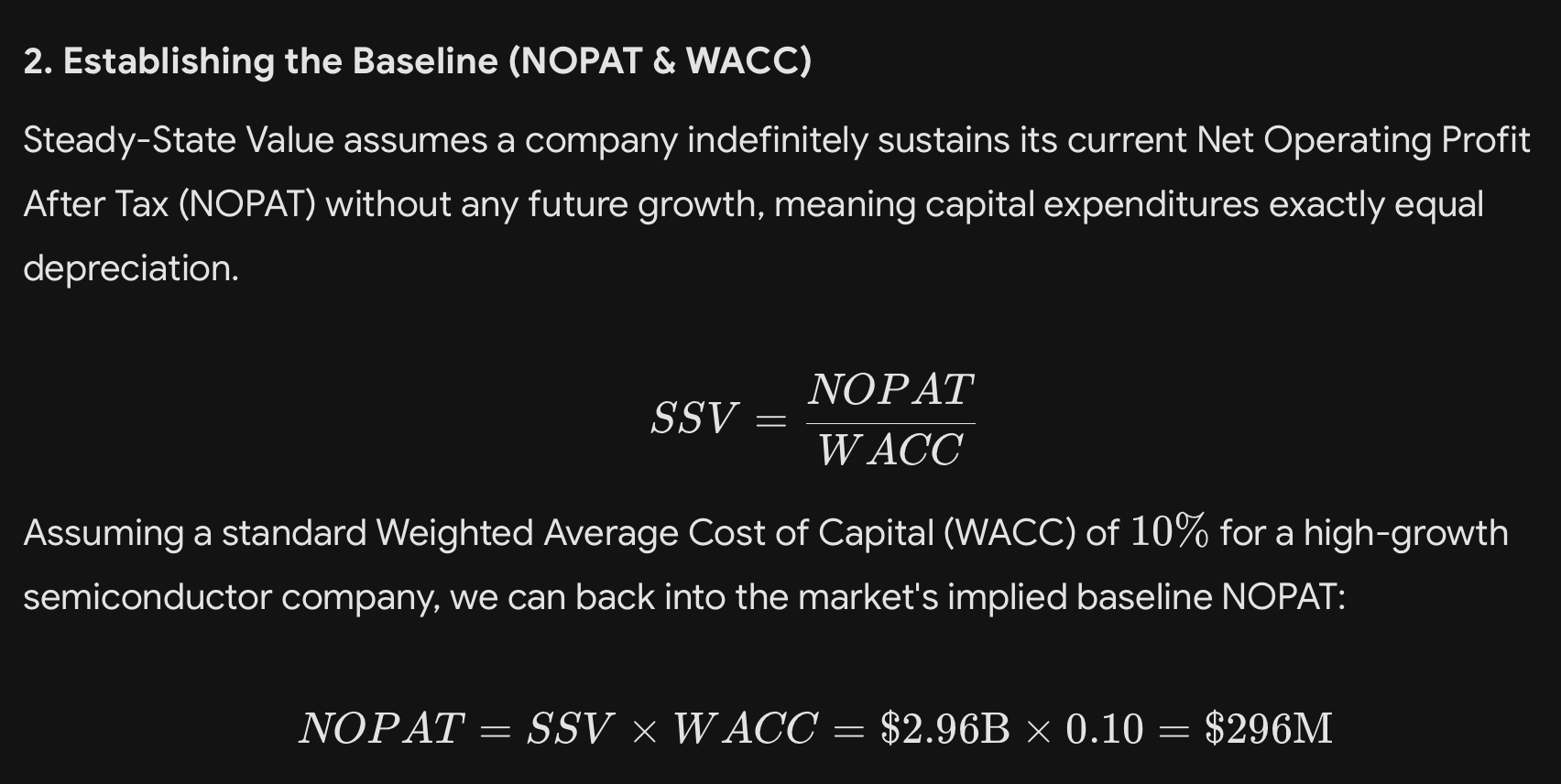

Steady-State Value: This assumes CRDO never grows again and just generates TTM NOPAT forever, discounted at 11%.

Steady State Value = $326M/0.11 = $2.96B

PVGO (Present Value of Growth Opportunities):

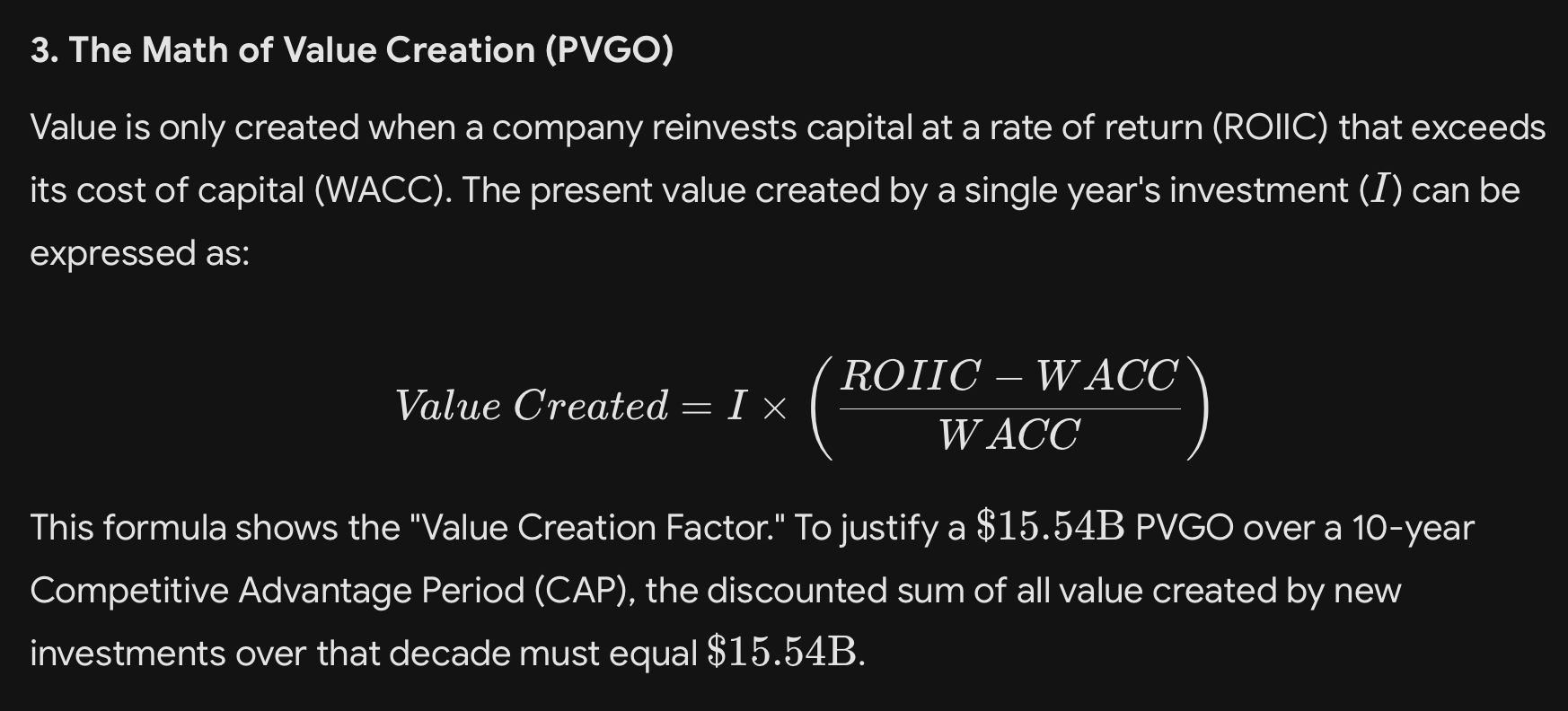

PVGO = EV− Steady State Value = $18.76 B−$2.96B = $15.8B

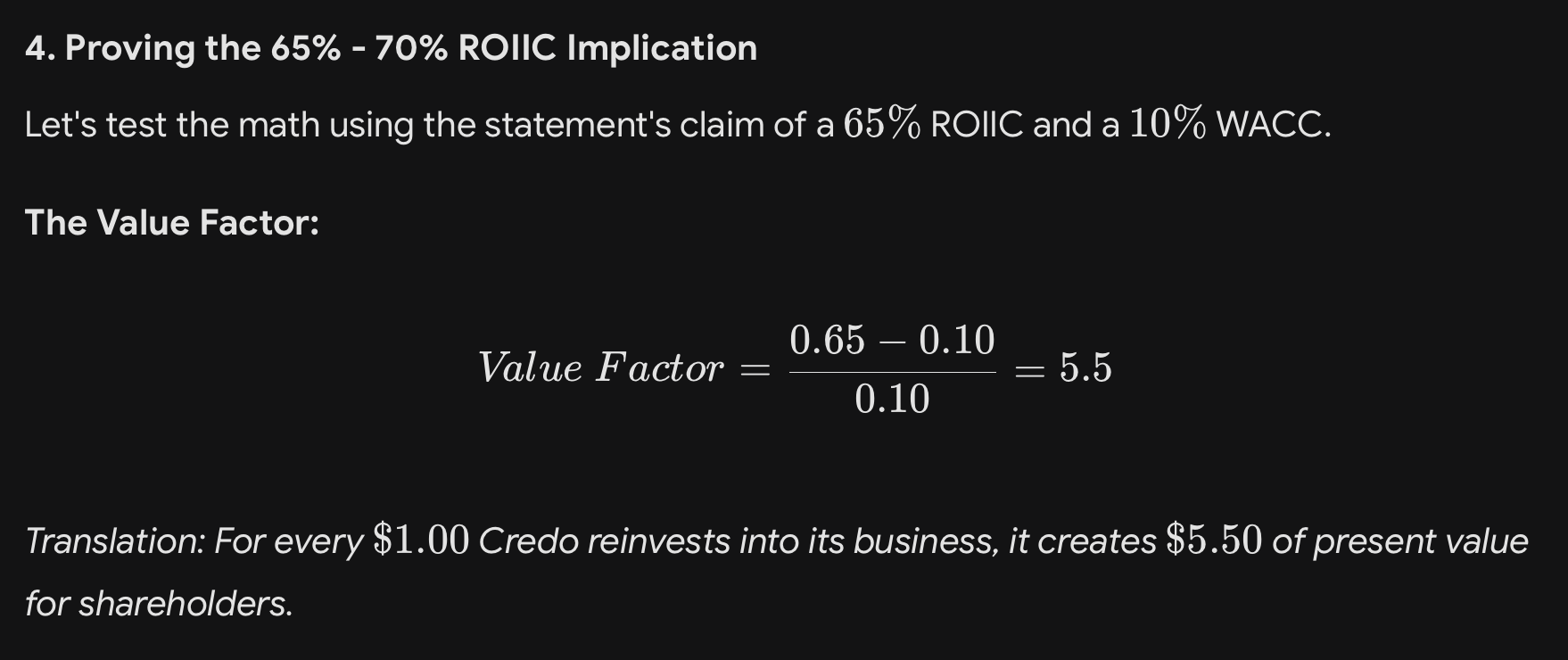

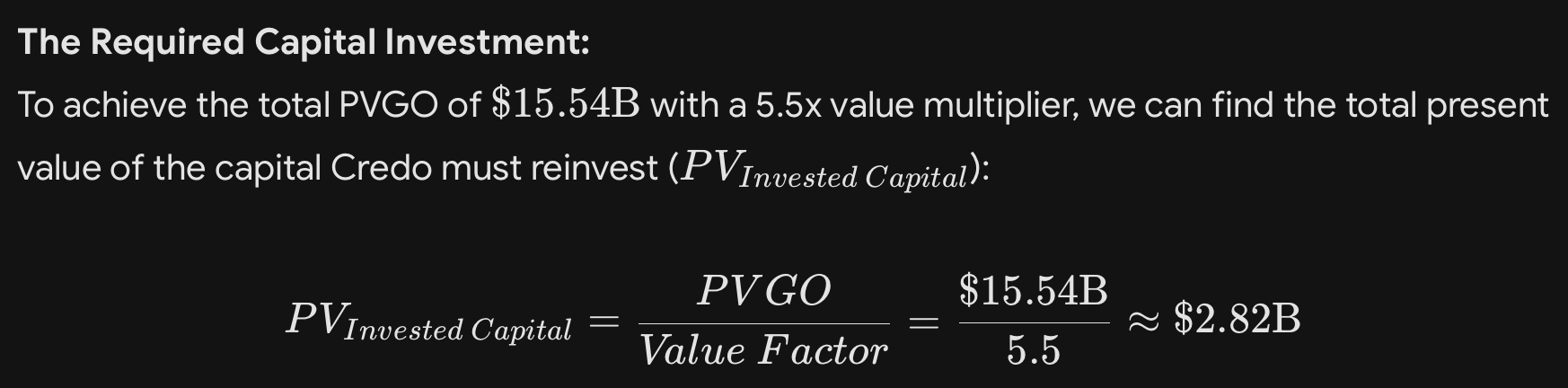

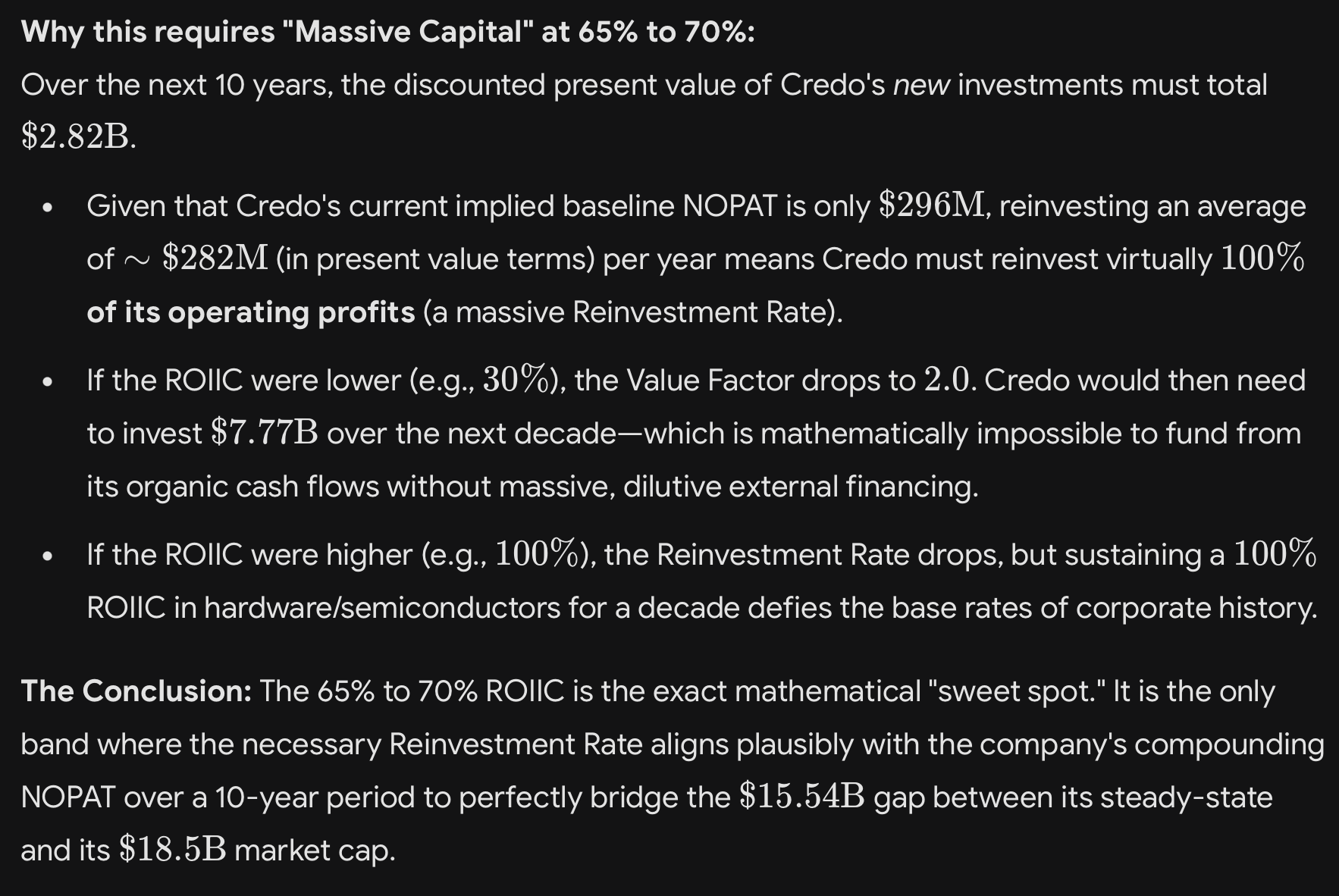

The MEROI Implication: PVGO accounts for a staggering 84% of Credo’s enterprise value. To justify this, the market’s MEROI expects Credo to reinvest massive amounts of capital at returns far exceeding the 11% cost of capital. Specifically, the current price implies a market-expected return on incremental investments of roughly 65% to 70% for the next decade.

Below is a step by step re-working of the MEROI calculation (note negligible difference in EV above and below due to shifting stock price):

Remember that SSV is the company’s value if it stopped growing today and the PVGO is the value of growth opportunities priced in via CRDO’s enterprise value. We are attempting to figure out what is priced in. Numbers like WACC are just assumptions and may not be dialed in but as always, these are thought experiments.

Tying it together:

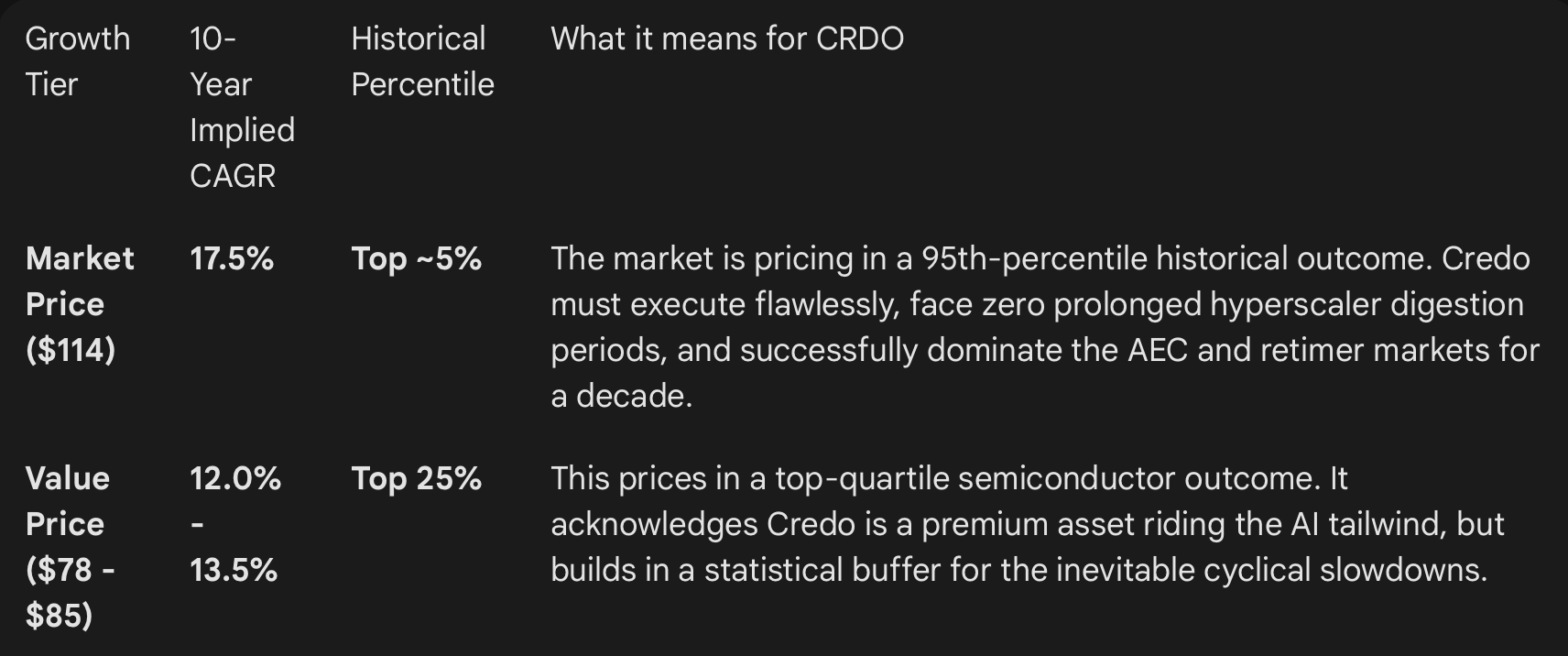

So to justify a stock price of $114 today, the market had priced CRDO to maintain a ROIIC of 65 to 70% for 10 years. Though it has achieved that in the triple digits for a year now, I can hear Aswath Damodaran, The Dean of Valuation, say “ok, it’s not impossible, that’s possible, but is it probable?”

Let’s revisit the bottom half my previous slide, tracking the PVGO and Implied 10-year FCF CAGR (or reverse DCF). At $114/share, CRDO’s PVGO is 84% of its EV and requires not only a 10 yr ROIIC of 65 to 70% but translates to a FCF CAGR of 17.5%

Anyone know if that is possible? Re-enter Mr. Mauboussin.

While financial databases do not isolate a universally published “10-year Free Cash Flow CAGR” specifically for the top quartile of semiconductors, analysts proxy this using long-term sales and earnings growth distributions, most notably from Michael Mauboussin’s The Base Rate Book and his subsequent research on intangible-heavy businesses. Note: I didn’t read the 215 pages and had to ask my quant. It is this aspect of my thesis that is weakest in that my conviction in this number from almost 60 years ago may not apply to a technological supercycle.

Here is the historical reality (3 main points) of what it takes to compound at those rates over a decade.

1. Mauboussin’s Base Rates for $1B+ Companies

To contextualize Credo’s 17.5% implied hurdle, we have to look at companies with a similar starting size. Based on Q4 guidance, Credo is approaching a ~$1.7B annualized run rate.

According to Mauboussin’s historical data (spanning 1950–2015) for companies starting with $1.25 billion to $2.0 billion in inflation-adjusted revenue:

The >20% Club: Only 3.0% of companies in this size bracket historically achieved a 10-year annualized growth rate greater than 20%.

The 15% to 20% Range: Achieving a ~17.5% CAGR over a full decade places a company roughly in the top 5% to 8% of all historical corporate outcomes.

The Median Reality: The historical base rate for median 10-year corporate growth sits in the mid-single digits (roughly 4% to 6%).

2. The Semiconductor Top Quartile

The semiconductor industry behaves differently than the broader market. Mauboussin’s updated 2021 research on intangible assets notes that tech and semiconductor firms possess higher median growth rates than capital-heavy industrials, but they come with a catch.

Top Quartile Base Rates: Historically, the top 25% of surviving semiconductor and semiconductor equipment companies achieve a 10-year FCF CAGR in the 11% to 14% range. This reflects the cyclical nature of the industry; explosive upcycles are inevitably diluted by inventory gluts and digestion periods.

The “Super-Compounders” (Top Decile): Companies that sustain 15% to 25%+ FCF growth over a decade (like Nvidia, TSMC, or ASML in their respective golden eras) do exist, but they are the extreme exceptions. They typically require a monopoly-like grip on a generational macro-shift (e.g., the build-out of mobile, cloud, or AI).

Higher Variance (The Penalty): Intangible-heavy semiconductor firms exhibit massive outcome variance. The risk of technological obsolescence is severe. For every Nvidia that compounds at 20%+, there are dozens of hardware companies that missed a product cycle and saw cash flows permanently decimate.

3. What This Means for Credo (CRDO)

When we apply these historical base rates back to the reverse DCF for Credo, the narrative becomes crystal clear:

In essence, owning CRDO at $114 is a bet AGAINST established base rates and that it is the next ASML, NVDA or TSMC. Even if you think it is a top 25% semi survivor (not just top quartile), the price at the time of writing of $98 has priced in another 20% premium and/or uncertainty. Part of that premium could be a compressed forward timeline with the first component of the OmniConnect ecosystem being released in May. One could also surmise that if the market has not (correctly) priced in Nvidia’s GTC unveilings on March 16th as it pertains to CRDO then there’s that too.

Considering the downside, the investor that bought at $114 is down 14% and risking a total of 29% loss if the median price of $81.5 is met. The “arithmetics of loss” I have covered in the past tells me that this is where decisions must be made from a long term capital preservation perspective. Deepening losses mechanically require much higher returns to break even. A buyer at $98 now would see a 17% loss at $81.5, which is manageable. This of course is not investment advice but an admonition/guideline where I make decisions.

Mauboussin and Damodaran would probably advocate for a probability band as to the outcomes. And here we don’t have an uber bull or significant bear case laid out while the two scenarios are relatively bullish.

Before my takes going forward, let’s summarize and mention the Competitive Advantage Period (CAP):

To understand why a stock with a 239% quarterly ROIIC and a 200%+ revenue growth rate can still violently sell off after earnings, we have to lean directly on the core tenet of expectations investing: Stock prices do not reflect current fundamentals; they reflect the market’s consensus expectations for the future.

A post-earnings sell-off in a high-flyer like Credo happens when the revisions to future expectations are negative, regardless of how spectacular the trailing 90 days were.

Here is the mechanical breakdown of why a sell-off occurs in this exact scenario:

1. Tripping Over the “MEROI Hurdle” (The Whisper Number)

We established that at $114/share, 84% of Credo’s Enterprise Value was Present Value of Growth Opportunities (PVGO). When a stock has an 84% PVGO, meeting Wall Street’s official consensus estimates is simply not enough. The stock is priced for perfection, meaning the buy-side “whisper numbers” are significantly higher than the printed estimates.

If Credo delivered a blowout quarter but guided the next quarter to “only” 30% sequential growth instead of the 40% the whisper number demanded, the implied 10-year CAGR we calculated (17.5%) gets revised downward by the market. When the growth rate drops in a reverse DCF, the multiple compresses instantly.

2. The “Duration of the CAP” gets Shortened

The Competitive Advantage Period (CAP) is the length of time a company can generate returns on capital that exceed its cost of capital. For Credo, the market has been underwriting a long, multi-year CAP driven by an uninterrupted hyperscaler AI buildout.

If management’s commentary during the earnings call hinted at any of the following, the market will immediately shorten its estimate of the CAP:

Customer Concentration Risks: A major hyperscaler (like Microsoft or Amazon) signaling a digestion period or a shift in network architecture.

Margin Peak: A warning that gross margins have topped out because the initial wave of high-margin premium AECs is giving way to more commoditized volume pricing.

Custom Silicon Threats: Hints that hyperscalers are aggressively developing in-house alternatives to Credo’s retimers.

Shortening the CAP mathematically destroys PVGO.

3. Exhaustion of Operating Leverage (Peak ROIIC)

Look back at the ROIIC chart. A jump from 161% to 239% is breathtaking, but it also triggers a forensic question: Is this as good as it gets? Markets are forward-looking mechanisms that constantly hunt for the second derivative (the rate of change). If the market believes 239% ROIIC is the absolute cyclical peak, then the rate of change going forward is negative. Deep-value and contrarian analysts actively look for these moments of peak cyclical margins to initiate short positions, knowing that gravity will eventually pull those returns back toward the cost of capital.

4. Crowded Positioning and Liquidity Extraction

Beyond the math, there are market mechanics at play. Heading into a highly anticipated semiconductor earnings print, positioning often becomes heavily skewed. Retail and institutional momentum is piled on one side of the boat (long call options, max-weight allocations).

When the news hits—even if it’s phenomenal—the “event” has passed. The liquidity generated by the earnings print provides the exact exit window that large funds need to unload shares without destroying the bid. The fundamentals didn’t break; the positioning just unwound.

The Bottom Line: A post-earnings sell-off isn’t a judgment on the quarter that just ended; it’s a recalibration of the decade ahead. The fundamentals generated the cash, but the valuation couldn’t support the weight of the expectations.

Conclusion:

I started off the post with my Latin teacher asking the question: “Credisne?” or “Do you believe?”. Do you believe that CRDO will make the optical transition with the same dominance and fashion that crowned it the defacto AEC king? Or is this c-suite desperation to squeeze everything from that “melting ice cube” as Nvidia and the AI Goliaths wrest back every advantage.

I believe CRDO is a well-run company whose engineers may not be one-trick ponies, whose CEO “did the right thing” and held a pre-announcement to tell shareholders that a re-rating was at hand, instead of a nasty surprise yesterday. Unlike other CEOs who will say “it’s ok (or) it will get better”, Mr. Brennan has had a plan in place and answered all questions as to what to expect. Credo, I believe, this company is doing the right thing.

Nonetheless, CRDO accelerating its OmniConnect release to May is a great defensive pivot, but surviving the optical transition against incumbents with vastly more R&D firepower—and deep, entrenched hyperscaler relationships—is a massive execution risk that deserves a higher discount rate.

I also believe in the investing math, base rates and what history says. Unless we believe that Credo is the next ASML, NVDA or TSMC; further downside should be respected if not expected. For me, if I had bought CRDO yesterday at $114, it is a SELL. If buying at $98 today, market indecision or a possible pending catalyst is worth a 17% premium; that opportunity cost is quite expensive, I would wait for clarity. Given the aforementioned catalysts and internal signposts, CRDO is on our Watch/Buy list. What one does of course depends on your situation and yes, your own personal credo.

Thanks for reading,

AlphaDoc

Disclosure: I am long ALAB, AMZN, ASML, AVGO, MSFT, NVDA and TSMC. As of this week I am/have been long put options on AVGO, CRDO and NVDA. I reserve the right to change these positions at any time without notice/update.

General Disclaimer: The information presented in this communication reflects the views of the author and does not necessarily represent the views of any other individual and/or organization. It is provided for informational purposes only and should not be construed as investment advice, a recommendation, an offer to sell, or a solicitation to buy any securities or financial products.

While the information is believed to be obtained from reliable sources, its accuracy, completeness, or timeliness cannot be guaranteed. No representation or warranty, express or implied, is made regarding the fairness and/or reliability of the information presented. Any opinions or estimates are subject to change without notice. The author’s opinion is subject to change at any time without prior notice or update.