Don't Get Wrecked By Soitec

There's Always A Bear Case Out There

“It ain’t what you don’t know that gets you into trouble. It’s what you know for sure that just ain’t so” - Popularly attributed to Mark Twain

Often times with a bullish narrative, the most important item missing is the key counterargument or the downside. Whether it is overriding bullish sentiment, the misattribution of risk or just the unknown unknown; experience has taught nearly all seasoned investors to factor in the bear case.

Jason’s Chips just penned “The Soitec Series | Part (1/7): Introduction to the French Photonics Substrate Monopoly”, an introduction to a lightly covered but possible semiconductor “pick and shovel” gem. Thank you to the author for apparently playing a role in getting Soitec some recognition . . . yes it seems a lot more people are paying attention:

The 3rd level thinking is that Soitec is a French toll-bridge technology provider in the semiconductor materials space, boasting a wide IP moat but suffering from acute cyclical whiplash. For those who have not heard me reference The 5 Levels of Thinking (adapted from poker to investing), please reference last year’s Broadcom (AVGO) article.

From my perspective, Jason’s Chips’ article comes down to 3 points:

Soitec's "Cornered Resource" as a French photonics substrate monopoly perfectly positioned to take significant share with the impending silicon photonics (SiPho) ramp-up.

Management's intentionally lowered guidance has created a temporary trust deficit but also a value dislocation where current multiples provide a tremendous margin of safety even if only one growth catalyst materializes.

A likely consilience of cyclical recovery and structural growth in 1.6T pluggable modules makes Soitec a strong multi-bagger play despite possible headwinds.

I also agree with most of his points, but with the nuance that they are “likely” even “probable” but the headwinds are not really priced in. This is where my variant perspective comes into play.

The bear case can be constructed as follows:

Soitec is mispriced by consensus as a cyclical recovery play. Forensic review of H1/Q3 FY26 filings and June 2025 broker notes indicates structural impairment across 70% of its revenue base. The core narrative—that end-market inventory will clear and historical 15% CAGR RF-SOI growth will resume—is factually broken by architectural workarounds at the foundry level and severe Chinese substrate commoditization.

Three Main Bearish Catalysts Not Covered:

SmartSiC CapEx Obsolescence: Brokerages zeroed out SmartSiC revenue models; EV OEMs are rejecting premium proprietary substrates as Chinese bulk SiC floods the market, stranding >€200M in Bernin 4 CapEx.

Mobile RF Content Reset: Structural RF-SOI content growth estimates per smartphone have compressed from 15% to 4–5%, mathematically precluding a return to Soitec’s historical >€1B revenue baseline.

Imager SOI Phase-Out: Tier 1 customers’ effective oligopsony and inevitable move away from 1st Generation Imager components is underway/under-appreciated by equity bulls

Below these are laid out like a short thesis dossier which I feel is the best visual framework.

Item 1 is a capital allocation and liquidity issue here noted as the SmartSiC “Stranded Asset” Disaster.

The Claim: SmartSiC will drive Automotive division hypergrowth for EVs.

The Reality: Automotive & Industrial revenue crashed 68% YoY in H1 FY26 to €11M (H1 FY26 PR, 11/2025, Pg. 3). Chinese competitors (e.g., SICC, TankeBlue) have rapidly scaled 200mm bulk SiC, destroying the pricing premium required to justify Soitec’s complex bonded SmartSiC process.

The Evidence: Management cited “longer than initially anticipated customer qualification cycles” resulting in a “delay in the expected wafer production ramp up by around two years” (Q3 FY25 Earnings Call, 02/06/2025, Transcript Pg. 4). Brokers have now removed 100% of SmartSiC revenue from forward estimates (Jefferies Equity Research, 06/13/2025, Pg. 1).

Financial Impact: The Bernin 4 facility, built specifically for SmartSiC via heavy FY23/FY24 CapEx, is operating at negligible utilization, crushing ROIC via unabsorbed D&A.

Item 2 is a customer and supplier risk: structural reset of RF-SOI content growth.

The Claim: Consensus assumed a 15% CAGR in RF-SOI content per 5G smartphone.

The Reality: Supply chain checks confirm handset OEMs have optimized RF front-end architectures, utilizing alternative packaging rather than expanding SOI wafer area.

The Evidence: Jefferies downgrade note explicitly states mobile RF content growth is now forecast at 4–5%, down from 15% (Jefferies Equity Research, 06/13/2025, Pg. 1).

Financial Impact: Q3 FY26 Mobile Communications revenue contracted 36% YoY to €90M. This is no longer merely “inventory digestion”; it reflects a structurally lower TAM (Q3 FY26 PR, 02/03/2026, Pg. 2).

Item 3 is very specific and most likely in my estimation but the timeline is vague and may be longer than the other 2: the Imager-SOI Phase-Out

The Claim: Soitec has sticky, recurring design-ins.

The Reality: A major Tier-1 US customer (inferred: Apple (AAPL)) is aggressively phasing out 1st-generation Imager-SOI.

The Evidence: H1 FY26 revenue for Edge & Cloud AI fell 14% YoY on a reported basis, explicitly driven by the “anticipated Imager-SOI phase-out” (H1 FY26 PR, 11/2025, Pg. 2).

Financial Impact: Immediate permanent loss of high-margin legacy revenue with “limited visibility into replacement sources” (Jefferies Equity Research, 06/13/2025, Pg. 2).

As a long term Apple shareholder, this is no surprise, in fact expected. AAPL CEO Tim Cook has been bringing their flagship product’s supply chain in house as much as possible and trying to bulletproof the manufacturing process. It’s not a matter of if but when.

There are 2 other issues that are related to the 3 above but bear mentioning as they were mentioned or implied in Jason’s article. Disclaimer (I had to reference Gemini Deep Research to get numbers and some of the rationale).

The worse may be yet to come, one way is in the form of further operating cash flow collapse.

The Claim: High structural EBITDA margins (>30%) protect the balance sheet during downturns.

The Reality: H1 FY26 Net Income dropped 582% YoY to -€33.35M. Cash from Operations crashed 79.79% YoY to €13.03M (Google Finance SOI:EPA data pull, 09/30/2025).

The Evidence: The company was forced to secure a €150M financing facility from the European Investment Bank (EIB) to maintain R&D commitments while simultaneously bleeding cash to redeem a €325M OCEANE 2025 convertible bond (H1 FY26 PR, 11/2025, Pg. 5).

Financial Impact: Net debt has increased to €443M (€1.26B total liabilities minus €823M cash equivalents). Interest coverage margins are compressing rapidly as EBIT turns negative.

Jason’s article mentioned governance only in that he believes that they released conservative guidance (“sandbagging”) in light of business headwinds as they pivot to Si-Pho opportunities. Below is albeit less specific but potentially more concerning with uncertainty that extends to the new CEO.

The Claim: Leadership is executing a known, multi-year strategic transition.

The Reality: CEO Pierre Barnabé abandoned the company exactly 38 months into his tenure, weeks before releasing the worst financial print in a decade.

The Evidence: Press release issued October 1, 2025: “Pierre Barnabé... has informed the Board of Directors of his intention to leave the Group for personal reasons” (Soitec AMF Filing, 10/01/2025, Pg. 1).

Analytical Inference: “Personal reasons” departures immediately preceding a 32% H1 revenue contraction historically correlate strongly with internal board disputes over unachievable forward guidance or impending asset write-downs.

I do not have any further insight other than wonder of the multiple issues: accountability, governance, culture or ethics? Perhaps Mr. Barnabé was a poor fit or got scapegoated. Not a good look for anyone involved when the differences could not be bridged until after earnings. A quick Google search reveals that there was drama when Barnabe was elected that points to underlying company culture/trust issues.

A Soitec investor must wonder what that means for his successor Mr. Rémont. Before assuming we are on to greener pastures, FWIW, Mr. Barnabé’s interests on paper were better aligned with shareholders as his equity compensation was 76% of his total pay, Mr. Remont’s is 43%.

One of the last things a company whose main business line is in a rut needs is c-suite theatrics/uncertainty; especially when there is recent history of same. Also consider this, Mr. Remont may want to clear the decks under the (bad) name of the last CEO, don’t be surprised if there is more unpleasant surprises next earnings. After all, it is all about expectations; and if you are starting from the bottom the only direction to go is up!

Now wouldn’t I be the pot calling the kettle black if in my bear case presentation I didn’t also state where these concerns fall apart?

I agree with most of Jason’s bull case and also what I quickly read about Archetypal Capital’s piece “Soitec. Is there operating leverage? What about valuation? What do the Fundamentals say?” Part of Archetypal’s article is paywalled but I think it is the valuation and conclusion section, I don’t think he directly addressed any of my bear case points either (but I would love to see them). Anyway, I digress.

This short thesis is invalidated if any of the following events occur:

Chinese SiC Embargo: The US/EU imposes draconian tariffs or outright bans on Chinese bulk SiC substrates, forcing STM and Infineon to pivot back to Soitec’s domestic SmartSiC supply.

Apple 5G mmWave Mandate: The iPhone 18 architecture unexpectedly pivots to a fully integrated 5G mmWave system-on-chip that mandates Soitec’s FD-SOI wafers universally across all SKUs, instantly reviving the Mobile division.

Photonics-SOI Hyper-Scale: The data center build-out for AI accelerates Photonics-SOI revenue to >€250M annually by FY27, masking the permanent decline in the RF handset business.

So that begs the question, what is my stance on Soitec? In our most aggressive portfolio, we are long Soitec but with a short leash. Those following me have heard me mention our pivot towards ex-US firms and Soitec fits that bill. The “Smart Cut” process with its now ~4300 patents is an impressive moat and the linchpin when it comes to our Helmer’s 7 Powers Analysis. Soitec has used this to develop a cornered resource that has transitioned into prodigious process power, switching costs and economies of scale. As this is not an in-depth article on SOI, I will move on to what made it a buy in light of the downside aforementioned.

Readers familiar with my schema know that a Mauboussin reference to “expectations investing” is inevitable. Of the myriad of metrics used to track and evaluate the current and future prospects of a company, one must go further than 1st order concepts like valuation and ROIC-WACC spreads. To determine if the future cashflows make sense in buying/holding a company today, it’s important to see what is priced in.

One critical set is the Return on Incremental Invested Capital (ROIIC) and Market Expected Return on Investment (MEROI). When the ROIIC is greater than the MEROI, said company may be creating value with their growth investments; when they are equal the company is breaking even and when ROIIC < MEROI then these growth investments are destroying shareholder value.

However, Soitec is currently enduring a severe inventory digestion cycle in its RF-SOI mobile segment, causing revenues to contract 29% organically in H1 FY26. Analyzing incremental returns during a cyclical trough artificially depresses the numerator (NOPAT) while the denominator (CapEx for future nodes) remains elevated.

Construct Definitions:

ROIIC (Return on Incremental Invested Capital): Measures the cash return generated by new capital deployed.ROIIC = ΔNOPAT/ΔIC

MEROI (Market Expected Return on Investment): Measures the economic spread of that incremental return against the cost of capital, dictating value creation. MEROI=ROIIC−WACC

Data Inputs (Estimated):

TTM NOPAT: ~€123M (EBIT of €149M taxed at Soitec’s 17.3% effective rate).

FY23 NOPAT (3 Years Ago): ~€220M (Peak cycle earnings).

Δ Invested Capital (3-Year): ~€300M (Aggressive cleanroom/capacity expansion).

Δ Invested Capital (TTM): ~€100M.

The Calculations:

3-Year ROIIC: ROIIC = (€123M−€220M)/€300M=−32.3%

TTM ROIIC: ROIIC = −€28M/€100M =−28.0%

Analytical Takeaway (MEROI): On a strictly trailing basis, Soitec’s MEROI is deeply negative. The company deployed hundreds of millions in CapEx to support a $2B revenue target just as the mobile end-market collapsed, resulting in negative ΔNOPAT.

However, Mauboussin warns against the “Denominator Blind Spot” in cyclical assets. Soitec’s core IP (Smart Cut) and gross margins have remained structurally intact (>30% EBITDA margins despite the volume collapse). When normalized for a mid-cycle recovery (assuming NOPAT recovers to €180M on the expanded €1.2B IC base), the forward MEROI is highly positive, driven by the extreme operating leverage of their fixed-cost fabs.

So a new wrinkle for even the regular readers, in cyclical companies a negative ROIIC must be viewed in context and a similarly negative MEROI signals not only (valuation) trough dynamics but also a potentially de-risked (hence bullish) setup. The corollary here is when a cyclical company is at peak earnings and a low PE, though optically cheap, it is expensive. Looking at Soitec’s PE, you get the converse scenario (optically expensive but potentially cheap):

So where does that leave us?

Well for those that actually do this for a living and know what they are doing (not me), they actually start figuring out the hard stuff: modeling the range of dossier impacts with probability bands/values as well as valuation.

Perhaps Archetype Capital sees fit to share what he has.

Sounds like Jason’s Chips will and perhaps also working in more of the risks if he agrees.

I will channel Morgan Housel: “The valuation of every company is simply a number from today multiplied by a story about tomorrow”. While we wait for Jason to tell us his story about tomorrow, here is what I can say I see today (again from Mr. Mauboussin). Note: the stock price used is from the last time I ran the numbers.

Reverse DCF: Expectations Investing

Rather than forecasting the future to guess the stock price, we reverse the Gordon Growth and DCF formulas to determine what free cash flow (FCF) growth rate is already embedded in the current €41.70 stock price.

Model Parameters & My Assumptions:

Enterprise Value: €1.58B

Discount Rate (r): 11%

Terminal Growth Rate (g): 3%

Normalized Base FCF: €100M. (Because TTM FCF is heavily distorted by the trough (-€47M) and FY25 was €26M, we must establish a mid-cycle baseline FCF of €100M to run a coherent growth model).

Solving for Implied Growth: We solve for g1, the 5-year FCF compound annual growth rate required to justify an EV of €1.58B, assuming it fades to a 3% terminal rate thereafter.

Result: A 5-year FCF CAGR of exactly 8.0% bridges the model perfectly.

Years 1–5 PV = €461M

Terminal Value PV = €1,122M

Total EV = €1,583M (~€1.58B target)

The market is pricing in an 8% FCF growth rate from a normalized €100M base. Given Soitec’s historical growth and its exposure to structural AI/data center tailwinds via Photonics-SOI, an 8% hurdle rate appears to be a low expectations bar, reflecting deep market pessimism regarding the current mobile inventory correction.

Keep in mind that Soitec’s actual historical FCF CAGR is spotty and the AI path is full of twists, turns and bottlenecks.

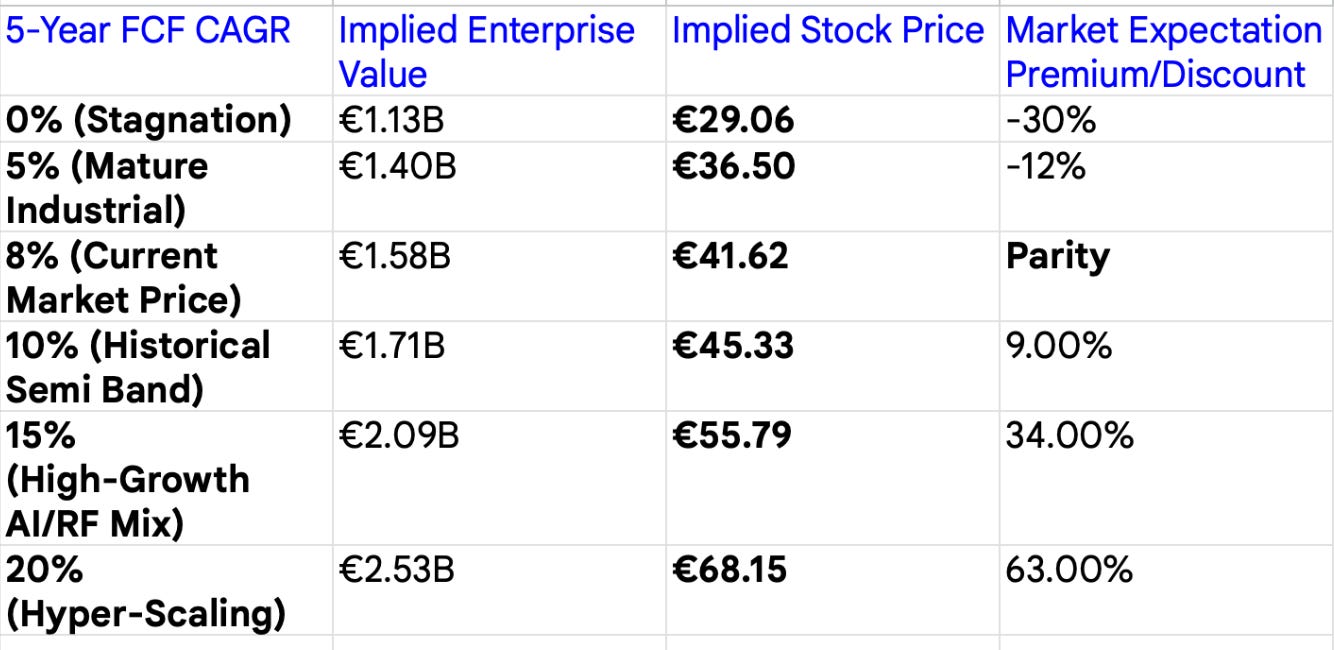

FCF Growth Sensitivity & Valuation Table

To assess asymmetric risk/reward, the table below sensitizes Soitec’s implied stock price against industry-banded FCF growth rates (assuming the same 11% WACC and 3% terminal rate over a 5-year explicit period on a €100M base).

With a closing price of €51.30 on March 11th, buyers at this level may be pricing in higher than average 5 year FCF CAGRs, significantly higher bar than just 24 hours ago. If Soitec matures into 5% FCF growth, the implied stock price is 29% lower.

This leads me to another (contrarian) observation. Jason and most SOI shareholders see a 20% jump in stock price and are more convinced that the thesis is proving out. It is likely that hedge funds and institutions are pulling price up. As a long term shareholder I would (like Buffett) prefer a lumpy 20% CAGR to a smooth 12% CAGR. However, with big money attention come big money problems.

Because institutions typically own 80 to 85% of the outstanding share float, they determine significant tops and bottoms. Some may argue price discovery, over a long period of time, holds better than these sudden spikes. Until we get better granularity on the speed and extent of the photonics catalysts, expectations are getting heady. Now the stock price moves more in sync with the Wall Street narrative than the underlying. The attendant volatility makes me believe it is all more important to know and understand the downside. We may think that Soitec with its impenetrable moat, is destined to succeed. It’s not that easy. Another lesson I learned from Mauboussin:

Never Underestimate The Red Queen.

From one of his many great missives, here “Underestimating the Red Queen

Measuring Growth and Maintenance Investments”:

“This topic is important because you can anticipate a company’s growth only if you understand how much capital the company spends on growth versus maintenance. A company’s prospects for growth may be dimmer than you believe if it is spending more on maintenance than you think.

In Lewis Carroll’s novel, Through the Looking-Glass, the Red Queen says, “Now, here, you see, it takes all the running you can do, to keep in the same place. If you want to get somewhere else, you must run at least twice as fast as that!”

Estimating maintenance capital expenditures provides insight into how fast a company has to run just to stay in place.”

I propose that the Market has either realizes its mistake and/or is pricing in a narrative that is not nearly as guaranteed. The easy money may already be over and challenging times ahead need conviction and result in tough decisions.

Are you ready?

This is where I have to leave it for now. Smarter people and those able to share their bear case targets may better inform us of the full investment case. I look forward to seeing/hearing more soon.

Thanks for reading,

AlphaDoc

Stellar article. Very in-depth. Thanks for sharing all this insight for free

This was written at 50€ per stock. We are now at 150 €. And we haven’t received a raised guidance or anything substantial. Crazy.